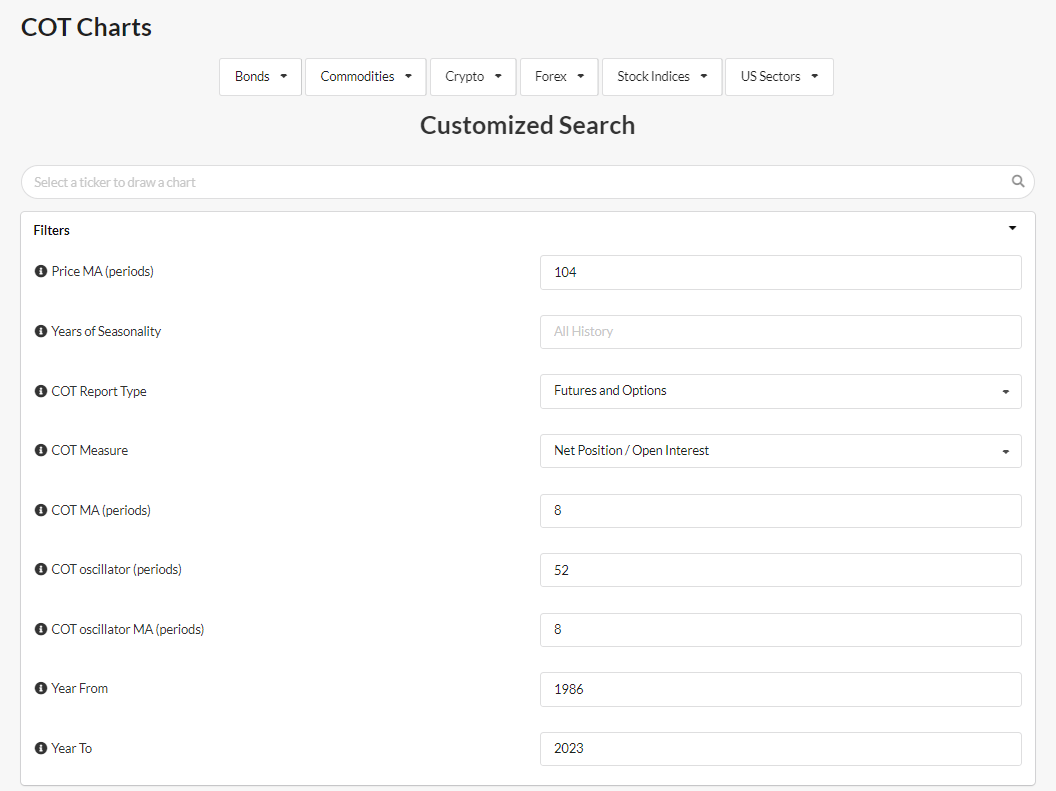

COT Filters

COT filters allow to customize the elaboration of raw COT-data. For example, to decide the Periods of the Indicators, and whether to apply Moving-Averages in order to smooth lines.

Below, a detailed explanation of each parameter. You can find the same information in the COT charts page, in the (i) info boxes.

- Price MA (periods)

- the n°of periods (in weeks) to compute the simple moving average over the price of the instrument.

- Trend is your friend, and Moving Average can be useful to determine it.

- The Moving Average will appear in the same sub-chart of the price.

- Example of Periods: 26w (6 months), 39w (9 months), 52w (1 year).

- Years of Seasonality

- the n°of years used to compute Seasonality. To use All-History available for an instrument, leave this field blank.

- it matters only if 'Show Seasonality' is selected from 'Chart Filters'.

- The algorithm computes the 'Detrended Seasonality' with a 'Rolling-Years' method. For example, if 'Years of Seasonality'=5:

- the seasonality of 2021 will be computed from 2016 to 2020;

- the seasonality of 2020 with the returns from 2015 to 2019;

- etc.

-

COT Report Type

It is a choice between:- Futures and Options: to see net-positions of operators for both Futures and Option Markets

- Futures only: to see net-positions of operators only for Futures Market

(This parameter is applied to both Legacy and Disaggregated raw-data and oscillators)

-

COT Measure

It is a choice between:- Net Position / Open Interest: to see the Net-positions of each group of operators as a percentage of the Open Interest

- Net Position: to see the Net-positions of each group of operators in dollars

(This parameter is applied to both Legacy and Disaggregated raw-data)

-

COT MA (periods)

- Is the number of periods of a Weekly Moving Average (MA) applied to COT-raw data (not oscillators).

- Moving average is useful to smooth the line, to reduce the noise and see the trend more clearly.

- For example, if 'COT MA'=8 ==> the last data of a COT group (e.g. Non-Commercials) will be the average of the last 8 observations

(This parameter is applied to both Legacy and Disaggregated raw-data)

-

COT oscillator (periods)

- It is the period, in weeks, used to compute the oscillators.

- For example, if 'COT oscillator'=52 ==> the oscillator will show how the group 'Commercials' is positioned today with respect to the 52 previous weeks.

(This parameter is applied to both Legacy and Disaggregated oscillators)

-

COT oscillator MA (periods)

- It is the n°of periods (in weeks) to be used to compute the Simple-Moving-Average over the COT oscillator data (e.g. over the Commercials Net-position oscillator).

- For example, if 'COT oscillator MA'=8 ==> the last data of a COT group oscillator will be the average of the last 8 observations

(This parameter is applied to both Legacy and Disaggregated oscillators)

- Year From

- the starting year of the Charts

- default is 12 years-ago

- Year To

- the ending year of the Charts

- default is the current-year